Does Homeowners Insurance Cover Plumbing Repairs?

Plumbing issues can be a nightmare for homeowners, leading to unexpected expenses and potential damage to your property. From burst pipes during cold winters to hidden leaks behind walls, plumbing problems can arise when you least expect them. If you find yourself facing such a situation, one of the first questions that may come to mind is, “Does homeowners insurance cover plumbing repairs?”

In this article, we’ll explore how your homeowners insurance policy responds to plumbing-related damages, from leaks and burst pipes to more complex issues. We’ll clarify what is typically covered under standard policies, what might not be, and how you can ensure you have the right coverage to protect your home. Whether you’re dealing with a sudden disaster or concerned about long-term plumbing issues, this guide will provide you with the information you need to make informed decisions.

This introduction gives readers an immediate understanding of the topic while ensuring that Google recognizes the relevance of the content to the search query.

What Plumbing Problems Are Covered by Homeowners Insurance?

Homeowners insurance generally covers plumbing problems that arise suddenly and unexpectedly. These incidents can cause significant damage to your property, and knowing what’s covered can help reduce stress when disaster strikes. Here are some common plumbing issues that most homeowners insurance policies will cover:

1. Burst Pipes

A burst pipe is one of the most common plumbing emergencies that homeowners face, especially during cold winter months. When pipes freeze and burst, the resulting water damage can quickly spread to floors, walls, and personal belongings. The good news is that homeowners insurance typically covers the damage caused by a burst pipe, including the cost of repairing or replacing damaged flooring, drywall, and personal property. However, it’s essential to check the policy exclusions, as some insurers may not cover damages caused by neglect or lack of maintenance.

2. Leaking Appliances

Appliance leaks can happen unexpectedly. Whether it’s a washing machine, dishwasher, or water heater, if an appliance leaks and causes water damage to your home, your homeowners insurance may cover the repair and cleanup costs. However, routine maintenance of these appliances is crucial, as wear and tear might not be covered. For example, if an appliance malfunctions due to lack of maintenance, the insurer may deny your claim.

3. Hidden or Undetected Water Leaks

If a plumbing leak occurs inside your walls or under your floors, it may go undetected for weeks or even months. Despite the damage being gradual, homeowners insurance often covers repairs related to hidden leaks. This includes the cost of tearing down walls to access the leak, repairing the plumbing, and restoring the area. However, as with other types of coverage, the leak must be sudden and accidental. Leaks resulting from lack of maintenance or gradual deterioration may not be covered.

4. Slab Leaks

Slab leaks occur when plumbing pipes beneath the concrete foundation of your home spring a leak. These types of leaks can lead to serious water damage and require immediate attention. Most homeowners insurance policies cover the cost of repairing the damage caused by slab leaks, including damage to flooring and the cost of accessing the pipes. However, repairing the pipes themselves might not be covered, depending on your policy’s terms.

By understanding the types of plumbing problems typically covered by your homeowners insurance, you can be better prepared to handle plumbing emergencies. While sudden and accidental damage is generally covered, it’s important to remember that every policy has its exclusions. Always review your policy and consult with your insurance provider to fully understand what’s covered and what’s not.

What Plumbing Problems Are Not Covered by Homeowners Insurance?

While homeowners insurance provides valuable protection, it’s essential to understand that there are certain plumbing-related issues that are not covered under a standard policy. Knowing these exclusions can help homeowners avoid unpleasant surprises when filing a claim. Below are some of the most common plumbing problems that homeowners insurance typically won’t cover:

1. Wear and Tear or Maintenance Issues

Homeowners insurance is designed to cover sudden and accidental damage, not wear and tear. If your plumbing system deteriorates over time due to lack of maintenance, age, or corrosion, the insurance company is unlikely to cover the repairs. For instance, if an old pipe bursts because it has been neglected or not properly maintained, the resulting damage is often excluded from coverage.

To avoid this, homeowners should regularly inspect their plumbing system and take steps to maintain it. Most policies will cover water damage from a burst pipe if it’s caused by a sudden incident, but damage resulting from neglect or preventable wear will not be covered.

2. Negligence or Failure to Act

If a plumbing issue is caused by your negligence, homeowners insurance typically won’t cover the damage. For example, if you leave your home for an extended period without turning off the water supply, and a pipe bursts while you’re away, the insurance company may deny your claim. This is because the damage was caused by your failure to take the necessary precautions to prevent the incident.

In cases where you notice a small leak but don’t act on it, or fail to properly winterize your home in freezing conditions, the insurance company may argue that the damage was avoidable and not covered under your policy.

3. Sewer Line and Sump Pump Failures

A standard homeowners insurance policy generally does not cover damage caused by sewer backups or sump pump failures. These issues are often the result of clogged sewer lines or an overwhelmed sump pump, and the damage they cause can be extensive. While water damage from a plumbing issue inside your home might be covered, backups and overflowing sump pumps are typically excluded.

To address this, homeowners can purchase add-ons or endorsements, such as water backup coverage, which can extend protection for these types of incidents. Without this additional coverage, homeowners may be left to handle the repairs and cleanup on their own.

4. Flood Damage

Flooding caused by weather-related events, such as hurricanes or heavy rain, is not covered under standard homeowners insurance. If the flooding damages your plumbing system, such as washing debris into your pipes or flooding the basement, this is typically considered flood damage and will not be reimbursed.

To protect against flood damage, homeowners can purchase separate flood insurance, either through the National Flood Insurance Program (NFIP) or private insurers. This will provide coverage for plumbing damage caused by flooding, but it’s crucial to have this coverage in place before the event occurs.

5. Plumbing Problems Caused by Tree Roots

If tree roots invade your plumbing system and cause a blockage or leak, most homeowners insurance policies will not cover the damage. This is often considered a maintenance issue and falls under the homeowner’s responsibility to prevent. While insurance may cover the water damage caused by the burst pipe, the cost of fixing the plumbing that was damaged by the roots will likely not be covered.

By understanding these common exclusions, homeowners can make informed decisions about the protection they need. Many of these issues can be prevented with routine maintenance and additional coverage options, ensuring your home and plumbing are adequately protected.

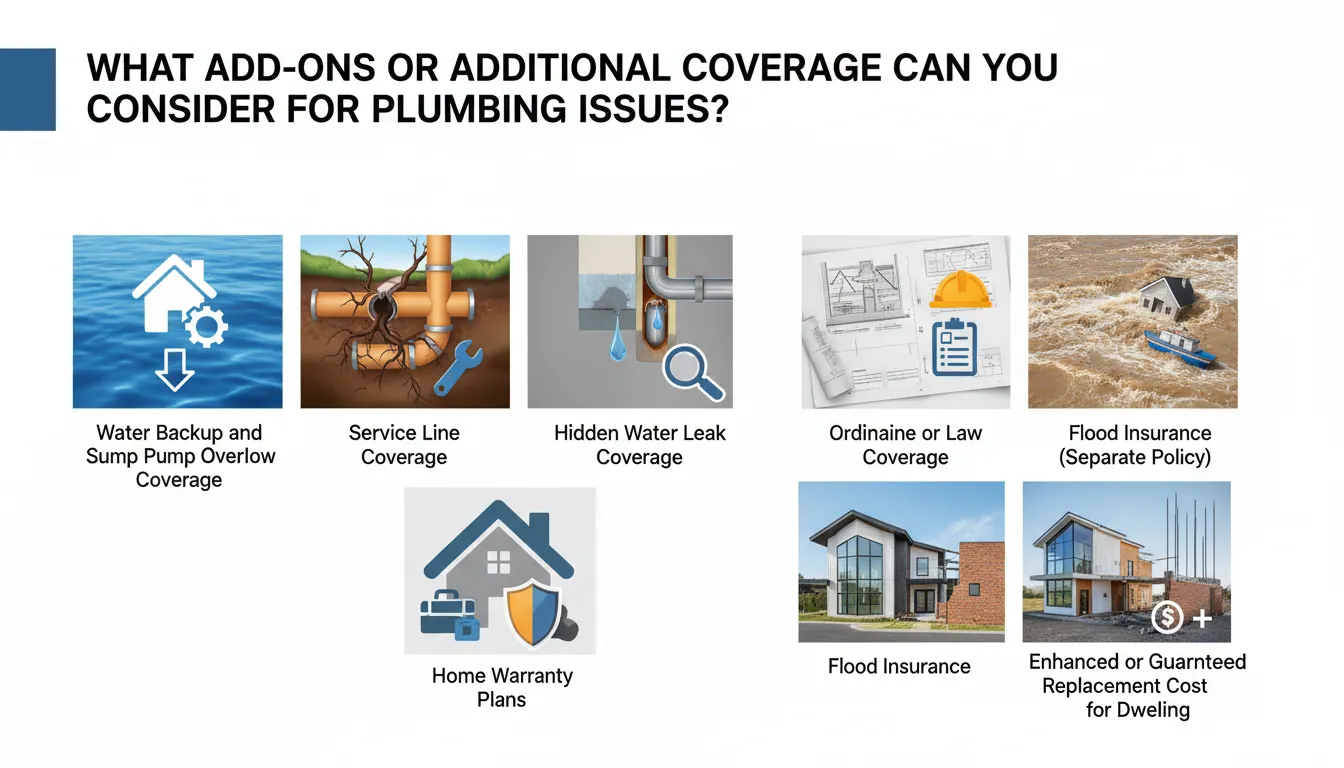

What Add-Ons or Additional Coverage Can You Consider for Plumbing Issues?

While homeowners insurance typically covers sudden and accidental plumbing damage, it often doesn’t extend to certain plumbing issues, such as sewer backups, sump pump failures, or mold caused by water damage. To bridge these gaps, homeowners can purchase add-ons or additional coverage options. Here are some of the most common and valuable options to consider:

1. Water Backup Coverage

One of the most important add-ons to consider for plumbing protection is water backup coverage. Standard homeowners insurance typically doesn’t cover damage caused by sewer backups, sump pump failures, or water backing up into your home. This can be especially problematic for homeowners with basements, where the risk of flooding or sewage backup is higher.

Water backup coverage helps pay for the cleanup, repairs, and restoration costs if water backs up from a sewer, drain, or sump pump. This coverage can be added to your homeowners insurance policy for a small annual premium, usually around $30 to $50 per year. For homeowners in areas prone to heavy rains or with older sewer systems, this coverage is highly recommended.

2. Service Line Coverage

Service line coverage is an add-on that covers the cost of repairs or replacement for broken utility lines running into your home. These include lines for water, steam, sewer, and drain systems that are outside your home’s foundation. While the plumbing inside your home is typically covered, repairs to these underground utility lines can be incredibly expensive, and most standard policies do not cover them.

Service line coverage is available as an optional endorsement and is usually priced at around $30 to $40 per year. This coverage can save you thousands of dollars in repair costs if a line breaks due to a covered peril, such as tree root intrusion, freezing, or other sudden events.

3. Mold Damage Rider

Water damage from plumbing issues can sometimes lead to mold growth in hidden areas, such as behind walls or under flooring. While homeowners insurance may cover mold removal if it’s caused by a sudden and accidental event, such as a burst pipe, coverage is often limited to a specific amount (usually between $1,000 to $10,000).

For homeowners worried about the potential for mold, adding a mold damage rider to their insurance policy is a smart move. This rider increases mold coverage limits and may extend protection to mold that grows gradually due to leaks that weren’t immediately detected. A mold damage rider can cost $50 to $200 per year depending on the policy and coverage limits.

4. Flood Insurance

Standard homeowners insurance policies do not cover flood damage, including water damage to plumbing caused by weather-related flooding, such as heavy rainfall, river overflow, or storm surges. If you live in a flood-prone area, such as a coastal region or a floodplain, flood insurance is essential.

Flood insurance can be purchased through the National Flood Insurance Program (NFIP) or through private insurers. This type of insurance covers plumbing damage caused by external water sources, such as flooding that enters your home and damages plumbing lines or appliances. Flood insurance is typically priced based on the flood risk in your area, with an average annual premium of $700 to $1,000, but it’s a small price to pay for the extensive protection it offers.

5. Equipment Breakdown Coverage

Although homeowners insurance may cover water damage caused by a malfunctioning appliance, it generally doesn’t cover the cost of repairing or replacing the appliance itself. If your water heater, dishwasher, or washing machine breaks down and causes water damage, you’ll likely need equipment breakdown coverage.

This add-on helps cover the cost of replacing or repairing major appliances that break down due to mechanical or electrical failure. It’s particularly valuable for appliances like water heaters and washing machines that are directly involved in plumbing systems. The cost of equipment breakdown coverage is usually around $50 to $100 per year, depending on the value of your appliances.

By adding these optional coverage options, homeowners can significantly enhance their protection against plumbing-related issues. These add-ons help fill in the gaps left by standard homeowners insurance and provide peace of mind knowing that you’re fully covered for unexpected plumbing disasters.

When Should You File an Insurance Claim for Plumbing Issues?

Dealing with plumbing issues can be stressful enough without the added complexity of filing an insurance claim. Whether it’s a burst pipe, a leaking appliance, or water damage, the decision to file a claim depends on several factors, including the severity of the damage, your deductible, and whether the issue is covered by your homeowners insurance policy. Here are some key considerations to help you determine when it’s time to file a claim for plumbing issues:

1. Assess the Damage vs. Your Deductible

The first step when considering whether to file an insurance claim for plumbing issues is to evaluate the extent of the damage and compare the repair costs to your policy’s deductible.

For example, if the cost to repair the plumbing damage is $800 but your deductible is $1,000, filing a claim may not make sense. You would end up paying for the repairs out of pocket, and your insurance company wouldn’t cover the damage since it’s below your deductible threshold.

If the damage is more significant, such as $5,000 worth of repairs for a burst pipe, it typically makes sense to file a claim, as the payout will exceed your deductible. However, keep in mind that every time you file a claim, your insurance premiums may increase, so it’s important to weigh the long-term cost of filing.

2. Is the Damage Caused by a Covered Event?

Not all plumbing issues are covered by homeowners insurance. If the damage was caused by lack of maintenance, negligence, or wear and tear, your claim may be denied. Homeowners insurance generally covers sudden and accidental events, like a pipe bursting due to freezing temperatures, but gradual damage or preventable leaks may not be covered.

To determine whether your plumbing issue is covered, carefully review your insurance policy and contact your insurance agent. If the damage is caused by a covered event, such as a burst pipe or a leak that occurred due to an unexpected event, you may be eligible for compensation.

3. Major Damage vs. Minor Damage

In some cases, the damage might be significant, but the cost to repair it is just slightly above your deductible. If this is the case, filing a claim may be worth considering. For example, if a burst pipe causes water damage to your walls and flooring, but the total repair costs are only slightly higher than your deductible, it might still make sense to file a claim if the costs to repair are significant enough.

On the other hand, for minor issues like a small leak under the sink, it may not be worth filing a claim. These types of minor repairs are usually better handled out of pocket to avoid increasing your premiums.

4. Is It a Recurring Issue?

If the plumbing problem is recurring or has been caused by an ongoing issue, such as poor maintenance or aging pipes, your insurance provider may deny the claim. Most insurance policies do not cover repeated incidents or issues resulting from neglect. In these cases, it’s better to fix the underlying cause of the problem before making a claim.

For instance, if your pipes have been leaking over several months and you’ve ignored the problem, your insurance provider might argue that the damage could have been prevented. In this case, it may be advisable to make the repairs yourself and address any preventative maintenance to avoid further damage.

5. Consider the Long-Term Impact on Your Premiums

It’s essential to consider the impact on your future premiums when deciding whether to file a claim for plumbing damage. Insurance companies often increase premiums after you file a claim, especially for water damage claims. If the damage is minor and the repair costs are near your deductible, it might be worth handling the issue without involving your insurance provider.

Before you file, it’s a good idea to contact your insurance provider to discuss the potential impact on your premiums. In some cases, the increase in your premiums might outweigh the benefit of receiving a payout for minor repairs.

By carefully considering these factors, homeowners can make an informed decision about when to file an insurance claim for plumbing issues. If the damage is significant, sudden, and covered by your policy, filing a claim may be the best option. However, if the damage is minor or the repair costs are close to your deductible, you may want to consider paying for the repairs out of pocket to avoid increasing your premiums.

How to Prevent Plumbing Problems in the Future

While homeowners insurance can help cover unexpected plumbing damage, the best approach is to prevent plumbing problems before they occur. Proactive maintenance and regular inspections can help identify potential issues early, saving you from costly repairs and insurance claims. Here are some essential steps homeowners can take to reduce the risk of plumbing problems in the future:

1. Conduct Regular Plumbing Inspections

Performing regular plumbing inspections is one of the easiest ways to catch issues before they escalate. Homeowners should check for common warning signs, such as:

Leaky faucets and pipes: Even a small drip can lead to significant water waste over time.

Corrosion or rust: Rusty pipes or fittings are more likely to fail and cause leaks.

Water pressure changes: Low water pressure can indicate a clog or leak in your pipes.

Unusual sounds: Whistling or banging sounds from pipes may suggest air in the system or a loose pipe.

It’s also a good idea to have a professional plumber conduct a yearly inspection, especially if your home is older or you live in an area with extreme weather conditions.

2. Insulate Pipes to Prevent Freezing

Frozen pipes are a leading cause of plumbing emergencies, particularly in colder climates. When water freezes inside a pipe, it can cause the pipe to burst, leading to water damage. To prevent this:

Insulate exposed pipes: Pipes in unheated areas, such as basements, attics, and crawlspaces, are at higher risk of freezing. Use foam pipe insulation or heating cables to protect these pipes.

Keep garage doors closed: If your garage contains pipes, keep the doors closed during cold weather to prevent cold air from reaching the pipes.

Let faucets drip: During extreme cold, allow a small stream of water to run from faucets connected to exposed pipes. This will help prevent the water from freezing.

3. Maintain Your Water Heater

Water heaters are an essential part of your plumbing system, but they can develop issues over time if not maintained. Regular maintenance can extend the lifespan of your water heater and prevent unexpected breakdowns. Here are some maintenance tips:

Flush the tank: Sediment buildup in your water heater can cause it to overheat and eventually fail. Flushing the tank annually removes this sediment and ensures efficient operation.

Inspect for leaks: Check the area around your water heater for signs of leaks, such as dampness or water pooling.

Adjust the thermostat: Set your water heater’s thermostat to 120°F to prevent scalding and reduce energy consumption.

4. Clear Clogs Regularly

Clogs are one of the most common plumbing problems. To prevent blockages and keep your plumbing running smoothly:

Use drain covers: Install mesh drain covers in sinks, bathtubs, and showers to catch hair, soap scum, and food particles that can lead to clogs.

Avoid pouring grease down the drain: Grease and fat can harden inside your pipes, causing blockages. Dispose of grease in the trash instead.

Use a plunger regularly: Periodically use a plunger on your drains to prevent buildup before it becomes a serious clog.

Perform a vinegar and baking soda treatment: Pour a mixture of baking soda and vinegar down the drain to clear minor clogs and freshen your pipes.

5. Maintain Your Sump Pump

A sump pump is a critical part of your plumbing system, especially in homes with basements prone to flooding. To keep your sump pump in good working order:

Test it regularly: Pour a bucket of water into the sump pit to test if the pump activates. If it doesn’t, inspect the pump for issues.

Clean the pump: Remove debris from the pump and the pit to ensure it operates efficiently.

Install a backup battery: During power outages, a backup battery for your sump pump ensures it continues working to prevent flooding.

6. Install Water Leak Detectors

Water leak detectors are a smart investment for homeowners who want to minimize the risk of water damage. These devices can be placed near vulnerable areas such as under sinks, around the water heater, or near appliances like dishwashers and washing machines. When the device detects moisture, it will send an alert to your phone, allowing you to take action quickly before the leak causes significant damage.

Some advanced models even allow you to shut off the water supply automatically when a leak is detected, providing an additional layer of protection.

7. Address Small Problems Immediately

It’s easy to ignore small plumbing issues, such as a dripping faucet or a slow drain, but these problems can lead to bigger, more expensive repairs if left unaddressed. It’s important to act quickly when you notice an issue:

Tighten loose fixtures: If you hear a drip, try tightening the faucet or replacing the washer.

Seal leaks: For small leaks, use caulk or plumbing tape to seal the gap temporarily until you can call a professional.

Fix running toilets: A running toilet can waste hundreds of gallons of water each day. If your toilet keeps running, it may be due to a worn flapper valve, which is easily replaceable.

8. Be Careful with What You Flush

What you flush down the toilet or drain can have a huge impact on your plumbing. Avoid flushing items that can cause clogs or damage your pipes:

Don’t flush wipes: Even “flushable” wipes can clog pipes and damage your septic system. Always dispose of wipes in the trash.

Avoid flushing paper towels, tissues, or cotton balls: These items don’t break down in water and can lead to blockages.

9. Maintain Your Gutter and Downspouts

Your gutters and downspouts play a critical role in keeping water away from your home’s foundation. Clogged gutters can cause water to pool around your foundation, leading to leaks and potential water damage inside your home.

Clean your gutters regularly: Make sure gutters are free of leaves, debris, and other blockages that can impede water flow.

Check downspouts: Ensure downspouts are directed away from your foundation to prevent water from accumulating near your home’s plumbing system.

By following these preventive measures, you can reduce the likelihood of costly plumbing issues and ensure your plumbing system remains in good working condition. Proactive maintenance not only saves you money on repairs but also helps prevent plumbing disasters from turning into insurance claims.

Conclusion & Final Thoughts

In conclusion, understanding how homeowners insurance covers plumbing issues is essential for homeowners who want to ensure they are adequately protected in the event of a plumbing disaster. Plumbing problems can occur unexpectedly, and when they do, the resulting damage can be costly. Homeowners insurance can provide valuable assistance in covering sudden and accidental damage, such as burst pipes and appliance leaks, but it generally does not cover routine maintenance or damage caused by neglect.

By knowing what is and isn’t covered by your homeowners insurance policy, you can make informed decisions about when to file a claim and when to handle repairs independently. Key factors to consider include:

The type of damage (sudden vs. gradual),

The cost of repairs relative to your deductible,

The cause of the damage (preventable or accidental),

The potential impact on your premiums after filing a claim.

Taking proactive steps to prevent plumbing problems is also crucial in avoiding future damage and insurance claims. Regular maintenance, timely repairs, and preventive measures such as pipe insulation and sump pump upkeep can save you from costly repairs and water damage in the future. Moreover, installing water leak detectors and maintaining your plumbing system will give you peace of mind, knowing you’re doing your best to prevent unexpected issues.

Final Recommendations:

Review your insurance policy regularly and consult your agent to ensure your plumbing needs are covered.

Perform routine maintenance and address minor plumbing issues promptly to prevent larger, more expensive problems.

Consider optional coverages like water backup or service line coverage to fill in gaps in your standard policy.

When disaster strikes, take swift action to minimize damage, document everything, and reach out to your insurance provider to file a claim when appropriate.

Remember, homeowners insurance is a tool designed to protect you from the unexpected, but prevention is always the best solution. Regular care and attention to your plumbing system can save you from the financial strain and stress that comes with plumbing disasters. By understanding your insurance coverage and taking preventive actions, you’ll be well-equipped to handle whatever plumbing challenges come your way.